The Channel Trap

Why Tupperware’s real mistake wasn’t plastic

Hey 👋,

I want to talk about something that bothers me.

Every time Tupperware comes up—and it comes up a lot now that the company has filed and collapsed—the take is the same: durable product, nostalgic brand, plastic went out of fashion, RIP. People say it like it’s a fun fact. Like the lesson is “don’t build something too good.”

That framing is wrong, and it’s wrong in a way that matters. Because the actual mechanism behind Tupperware’s collapse is alive and eating several multi-billion dollar companies right now. And those companies are getting the same polite, useless coverage Tupperware got for a decade before it finally filed Chapter 11 in September 2024 with $800 million in debt and no real plan.

So let’s do this properly.

In partnership with

Launch fast. Design beautifully. Build your startup on Framer—free for your first year.1

First impressions matter. With Framer, early-stage founders can launch a beautiful, production-ready site in hours. No dev team, no hassle. Join hundreds of YC-backed startups who launched here and never looked back.

One year free: Save $360 with a full year of Framer Pro, free for early-stage startups.

No code, no delays: Launch a polished site in hours, not weeks, without hiring developers.

Built to grow: Scale your site from MVP to full product with CMS, analytics, and AI localization.

Join YC-backed founders: Hundreds of top startups are already building on Framer.

The Original Insight Was Good

Earl Tupper was a Massachusetts businessman who figured out, post-WWII, how to turn polyethylene slag—industrial waste nobody wanted—into a new kind of plastic he called Poly-T. Lighter, tougher, genuinely innovative. He made bowls with airtight lids that needed to be “burped” to seal.

Nobody bought them. Department stores couldn’t sell them. Consumers in the late 1940s thought plastic meant cheap and smelly, and the burp mechanism just confused people. The product was real but the product couldn’t sell itself.

Enter Brownie Wise—divorced, cash-strapped, former secretary—who’d been running a direct-sales side hustle and figured out something important: the home party wasn’t about the product. It was about the room. You got housewives buying things alongside their friends instead of from a stranger at the door, you created trust, demonstration, community. Wise launched Patio Parties, threw the bowls across the room to prove they wouldn’t shatter, turned the confusing burp into a ritual. By 1951, Tupper made her VP of Tupperware Home Parties. By the time the company went public in 1996, it was in nearly 100 countries.

Here’s the thing though—and this is the part everyone skips.

The moat was never the product. The containers were good, but they weren’t irreplaceable. The moat was the distribution. The party created trust and provided a live demo for something that desperately needed one. Take that away, and you have a decent plastic container in an aisle next to twelve decent plastic containers, with no story and no reason to cost more.

This is what I’d call the first law of the channel trap: when your competitive advantage lives in how you reach the customer and not in what you’re selling, you are one disruption away from having nothing.

Tupperware had a distribution business that sold containers. It thought it had a container business. Those are different things.

The Consultants Become The Veto

Here’s where it gets uncomfortable.

By the time Tupperware’s leadership understood what was happening—e-commerce maturing, younger consumers not showing up, the party model declining—they had 465,000 freelance consultants whose livelihoods depended on direct sales continuing to exist. Many of them were women in developing markets who had built real businesses on the Tupperware platform. Real businesses. Real income.

This is not “an anchor.” This is Clayton Christensen’s Innovator’s Dilemma wearing a human face.

The moment leadership seriously pivoted to retail and e-commerce, they were explicitly telling nearly half a million people that the model they’d built their livelihoods around was over. So they didn’t say it. They launched on Amazon and Target in 2022 while trying not to alarm the consultants. They attempted to do both.

You cannot quietly cannibalize your own distribution channel. The consultants noticed. Active sellers dropped from roughly 600,000 to 284,000 in just a few years. The company’s own regulatory filings called it a “sharp decline.” They’d spooked the old model without building the new one.

Newspapers couldn’t kill print. Kodak couldn’t cannibalize film. Tupperware couldn’t betray its salesforce. Same movie, different decade.

The consultants were the asset and the veto simultaneously. By the time management accepted the old model was over, they were years behind every competitor who’d built e-commerce from scratch. And the debt—which had swollen past $800 million—had no patience for a slow transformation.

The Part That Actually Hurts

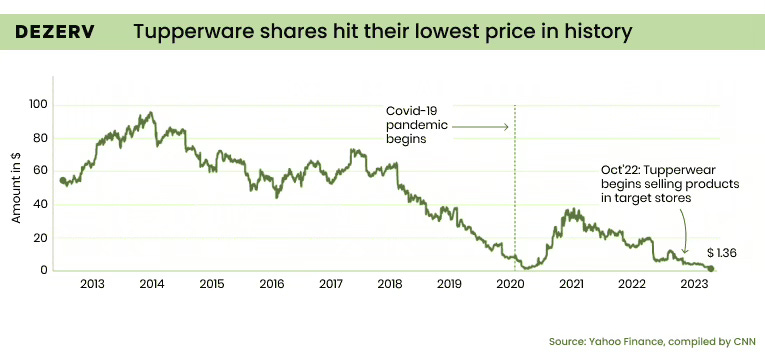

In early 2020, Tupperware was already dying. Stock in freefall, cycling through CEOs, no coherent strategy.

Then the pandemic hit and everyone started cooking at home.

Tupperware’s profits quadrupled. The stock shot up nearly 3,000%. Consultants pivoted to Zoom parties. Management looked at this and called it a turnaround.

It wasn’t. It was a temporary demand spike from people stuck at home—nothing to do with strategy, nothing to do with the underlying problems getting fixed. The party model was still eroding. The brand still wasn’t landing with anyone under 40. Plastic was still becoming a cultural villain. The structural problems were exactly where they’d been before COVID, except now the company had less time and more debt.

Q1 2022: spike over, guidance withdrawn, stock down 45%, CFO flagging material weaknesses in financial controls.

The pandemic was probably Tupperware’s last real window. A moment of genuine attention and cash that could have funded new materials, new channels, a real pivot. Instead, leadership concluded the turnaround had already happened.

This is what I mean when I say the framing matters. “Tupperware died because plastic went out of fashion” is not a useful lesson. “Tupperware had a clear window, misread a cyclical spike as a structural fix, and burned the remaining time” — that one you can actually do something with.

This is where the story stops being history.

Herbalife does $5 billion a year in nutrition products through a direct-sales network of 2.1 million distributors. Sales fell in 2022, 2023, and again in 2024. The company launched “Nutrition Clubs”—physical locations owned by distributors—which turned out to attract retail customers who just wanted to buy a shake, not join the business. The company’s own president said club conversion from customer to distributor runs at 1-2%. That’s not a pipeline. That’s a structural leak dressed up as a retail strategy.

Medifast—direct-sales weight management, meal replacement coaches as the entire channel—has been in freefall since GLP-1 drugs like Ozempic went mainstream around 2023. Revenue dropped another 36% in 2025, falling to $385.8 million from $602.5 million the year before. The company posted an $18.7 million net loss. The coaches didn't stop working. The category they were selling into just evaporated—people suppressing appetite with a weekly injection don't need a meal replacement program, a personal check-in, or a system. Different product. Exact same structural problem: the channel was the moat, the channel's market disappeared, and there was no product underneath it strong enough to survive on its own.

The pattern is identical to Tupperware’s, just playing out faster because the disruption is sharper.

Mary Kay. Nu Skin. Amway. All of them sitting on direct-sales dependencies built for a distribution environment that no longer exists, all of them showing some version of the same metrics: declining active sellers, flat or falling revenue, pivots to “omnichannel” announced several years too late.

The common thread isn’t plastic. It’s the channel being the moat—and the channel eroding.

SaaS companies built their entire go-to-market on a channel: the sales rep. Enterprise software doesn’t sell itself—you have a massive inside sales team, SDRs cold-calling, account executives doing demos, customer success managers holding the relationship. The channel is the moat. Salesforce didn’t win because their CRM was so much better than everything else. They won because they built the most aggressive, most trained, most incentivized sales force in software history.

Now AI is eating the channel from both ends.

On the buying side: companies are cutting software spend because AI can replace what the software was doing. Why pay for a $50k/year contract management SaaS when your legal team is just using Claude? The category evaporates, same as Medifast.

On the selling side: the SDR role—the bottom of every SaaS sales org—is getting automated. The humans who built careers as the distribution layer for enterprise software are being replaced by AI outreach tools. The channel is thinning out.

The trap for big SaaS incumbents is exactly Tupperware’s dilemma: their sales reps are the asset and the veto simultaneously. You can’t quietly tell 10,000 account executives that AI is replacing their workflow while asking them to keep closing deals. So companies are doing both badly—launching AI features to justify contracts while pretending the sales motion is unchanged.

The companies most exposed are mid-market SaaS—too big to be nimble, not sticky enough to survive category erosion, entire revenue model built on a human sales channel that’s becoming optional.

The Mechanism

Pull it apart and you get four moves that always seem to happen in order.

The channel becomes the moat. A company builds its advantage not in the product but in distribution. Works spectacularly. Community, trust, barriers to entry—all baked into the sales model. The product is almost incidental.

The channel becomes the customer. Over time, the real product isn’t containers or supplements. It’s the business opportunity the channel offers its participants. The salesforce stops being a distribution network and becomes the actual customer base—with needs that start to diverge from end consumers.

The channel becomes the veto. Disruption arrives. The company can’t respond because responding means telling the people who built the business that their model is dead. So it compromises—tries to do both, fails at both, burns time.

The window opens and closes. There’s usually a moment when transformation is actually possible: a demand spike, a leadership change, a genuine crisis that creates political cover. It requires someone to stand up and say the old model is over. Most companies can’t do it in time.

The escape—when companies manage it—usually looks like one of three things: a new channel built to be additive rather than competitive (rare), a separate brand for the new model so existing consultants don’t see it as an attack (very hard), or using a genuine crisis as cover to rip the bandaid when the cost of staying still finally outweighs the cost of change.

Tupperware never got there. The Tupperware Brands Corporation is gone—stock delisted, employees laid off, 78-year-old public company dissolved.

The brand is technically alive. A shell company called Party Products LLC—formed by the same distressed debt investors who bought Tupperware’s loans at pennies on the dollar, triggered the bankruptcy, then credit-bid the brand out of is—now owns the name and operates in eight core markets. They’re calling it a “startup mentality” rebuild. The CEO is the same. The language is the same “digital-first, asset-light” framing that didn’t work before.

And then in January 2026, Party Products announced it was selling Latin America—Tupperware’s strongest market, $404 million in sales as recently as 2022—to Betterware de México for $250 million. Deal not yet closed, pending regulatory approval. Party Products framed it as “focusing on core markets.” What they’re actually doing is selling the best-performing region for cash while holding onto the parts that need the most work.

Europe is gone. Most of Asia is gone. Latin America is being sold. What remains is a brand being unwound piece by piece by the people who got it in a bankruptcy credit bid.

This is a salvage operation. There is a meaningful difference between a company being rebuilt and a brand being sold for parts—and right now Tupperware is the second thing. The distressed debt investors converted their loans to equity and are now systematically converting that equity back to cash. That’s their business model. It’s a legitimate one. It just has nothing to do with building anything.

Which is, honestly, the sharpest version of the lesson: if you wait long enough to admit the channel model is broken, the only people who want to own the brand are people who make money from broken things.

The window is open.

It won’t stay that way.

Thanks for reading.

If you enjoyed this issue, send it to a friend—it helps more than you think.

Back in your inbox Friday,

Kenneth F.

Eligibility: Pre-seed and seed-stage startups, new to Framer.